In the world of trucking, the weight of financial obligations can feel insurmountable, especially when it comes to truck payments. Missing just one or two payments can trigger a cascade of anxiety, leaving fleet managers and operators grappling with the looming threat of repossession. The risks involved in defaulting on payment are not only financial; they embody the fear of losing a critical asset that drives your operations forward. As you navigate these turbulent waters, understanding the repossession process within the trucking industry becomes paramount. This process is often fraught with emotional turmoil, as a truck is not just a machine-it’s a lifeline, a source of livelihood, and a vessel of dreams for many entrepreneurs in logistics and freight. To combat this stress, being informed and prepared can make all the difference in safeguarding your investment and your peace of mind. Learn more about budgeting for routine truck maintenance.

Understanding the Repossession Process

The repossession of vehicles is a serious matter that can have significant implications for businesses, particularly in the trucking and logistics sectors. Understanding how this process works, along with its legal framework, is vital for any fleet manager or business owner.

What is Repossession?

Repossession occurs when a lender takes back a financed vehicle after the borrower fails to make their payments. This can happen after missing just one or two payments, depending on the terms of the loan agreement. According to the Consumer Financial Protection Bureau, lenders are allowed to repossess vehicles without notice in most situations, but they must adhere to specific legal requirements to ensure the process is conducted lawfully.

Legal Aspects of Repossession

The legal framework governing repossession predominantly falls under the Uniform Commercial Code (UCC). It stipulates that lenders may reclaim their collateral after a borrower defaults. Importantly, the lender must notify the borrower of the missed payments and provide them a reasonable period to remedy the default – typically a few weeks. Moreover, lenders cannot use force or threats when repossessing a vehicle. They must conduct the action in a manner that does not breach the peace, according to state laws. For further details on state-specific laws, check NerdWallet’s guide.

Emotional Implications for Businesses

Facing repossession can lead to significant emotional stress for business owners. It often represents not only a financial loss but also a personal failure, invoking feelings of embarrassment, guilt, and anxiety. Owners may worry about the impact on their reputation, particularly in industries where reliability and trust are paramount. This mental burden can affect decision-making and overall business health, as indicated in an article about the emotional price of failure.

In conclusion, understanding the repossession process and its implications can help fleet managers and trucking business owners take preventive measures and make informed decisions.

Truck Repossession Laws Comparison

Understanding the laws regarding truck repossession is crucial for fleet managers, trucking company owners, and operators in the logistics sector. The notice periods and unique state requirements can greatly affect your operations and contractual obligations. Below is a table comparing truck repossession laws across several states:

| State | Notice Period | Unique Requirements |

|---|---|---|

| California | 10 days written notice | Must provide written notice; repossession agents cannot enter private property without permission or use force. |

| New York | Immediate repossession allowed | Prohibits repossession between 9 PM and 7 AM; repossession must be conducted peaceably. |

| Texas | No notice required | Repossession agents may not use force, threats, or enter a home; must remain peaceful and non-disruptive. |

| Florida | 48 hours notification after repossession | Borrower has right to redeem the vehicle by paying the full balance plus fees within a specified period post-repossession. |

For further reading on financial planning in trucking, you can learn more about building an emergency repair fund and optimizing fleet size and maintenance for your company.

Impact of Missed Payments

Missing truck payments can have profound financial and operational consequences for fleet managers and trucking company owners. Understanding these ramifications is crucial in preventing long-term damage to your business. Here are key impacts of missed payments:

-

Immediate Financial Consequences:

-

Missing a payment can trigger late fees, increasing your overall debt.

-

Continuing missed payments can lead to the lender initiating repossession after 60-90 days, resulting in losing the vehicle.

-

Damage to Credit Score:

-

Even a single missed payment can lead to a significant drop in your credit score, potentially reducing it by 100 points or more, impacting your future borrowing capacity.

-

Late payments typically remain on your credit report for up to seven years, making it harder to secure favorable loan terms in the future (source).

-

Operational Disruption:

-

Repossession of equipment can disrupt freight schedules and client contracts, leading to potential loss of business and reputational damage.

-

Loss of a truck means reduced fleet capacity, making it difficult to meet delivery commitments.

-

Increased Difficulty in Obtaining Future Financing:

-

A negative mark on your credit file can lead to higher interest rates and stricter loan terms from lenders, limiting your ability to invest in new vehicles or equipment (learn more about truck financing).

-

Risk of Legal Action and Deficiency Balances:

-

If the repossessed vehicle is sold for less than what you owe, you may still be responsible for the remaining balance, putting further financial stress on your business (source).

In conclusion, staying on top of loan payments is essential not just for maintaining good credit but also for ensuring the smooth operation of your fleet.

Case Study: Impact of Missed Payments Leading to Repossession

Introduction

In the volatile world of fleet management, unexpected financial troubles can devastate even the most well-planned operations. This fictional case study focuses on a mid-sized trucking fleet that faced the heart-wrenching consequence of vehicle repossession due to missed loan payments.

The Background

Fleet Name: Reliable Haulers, Inc.

Location: Oklahoma

Fleet Size: 20 trucks, including Class 8 tractors and delivery vans

Loan Amount: $350,000 for fleet expansion

Payment Terms: Monthly installments over 5 years

Reliable Haulers, Inc. was once a thriving trucking company known for its dependable service and growing clientele in logistics and freight delivery. However, rising operational costs and unexpected delays in freight payments from clients led to cash flow challenges. Despite their efforts to cut expenses, they regrettably missed three consecutive loan payments on their truck financing agreements, triggering the risk of repossession.

Emotional Impact

The emotional toll of impending repossession weighed heavily on Mike, the fleet manager. He had dedicated years to building the company and fostering a loyal team. The fear of losing the fleet meant not only the loss of equipment but also the potential job losses of his employees, many of whom depended on their salaries to support families.

“Every missed payment felt like a rock in my stomach. The thought of losing everything I worked for was unbearable,” Mike shared during an emotional recount of the situation.

The psychological burden was compounded when local competitors began discussing the company’s struggles, leading to a loss of morale among employees and lingering worries about their future. Mike often found himself working late nights, exhausted and overwhelmed by the fear of repossession, knowing every day he delayed addressing the issue brought them closer to the edge.

Financial Impact

The missed payments eventually culminated in repossession when the bank initiated proceedings after the stipulated cure period of 30 days expired. Despite attempts to negotiate a modified payment plan, the lender opted to reclaim the vehicles, citing a lack of confidence in future payments. Reliable Haulers lost significant assets as 10 of its trucks were repossessed, resulting in the following financial implications:

- Asset Loss: Loss of $300,000 worth of vehicles, impacting operational capacity and service capabilities.

- Credit Score Decline: The repossession substantially reduced the company’s credit score, complicating future financing.

- Increased Operational Costs: The remaining fleet experience increased operational pressures, as fewer trucks meant higher workloads per vehicle, resulting in costly maintenance issues and strained resources.

Lessons Learned

This case exemplifies the critical importance of managing cash flow and establishing contingency plans for unexpected downturns. After experiencing the trauma of repossession, Mike and his team prioritized improving their financial literacy and communication with lenders. They sought to establish an emergency repair fund and devised a budgeting model that accounted for seasonal fluctuations in income.

Reliable Haulers now emphasizes preventive financial planning in their operations. Mike also shares his story with local fleet operators, advocating for the necessity of maintaining open communication with financial institutions to negotiate plans before defaults occur.

Conclusion

The experience of Reliable Haulers, Inc. serves as a cautionary tale for fleet managers and trucking company owners. Understanding how many truck payments can be missed before repossession varies by lender, often hovering around two to three missed payments. While it can be easy to overlook small cash flow issues, proactive management and communication could prevent disastrous consequences.

Learn more about maintaining a successful fleet and strategies for establishing an emergency fund to safeguard against financial emergencies.

In the realm of vehicle financing, understanding when missed payments can lead to repossession is critical, particularly for fleet managers, trucking company owners, and other industry stakeholders. Financial experts agree that the repercussions of payment delinquencies can manifest sooner than one might expect.

Key Findings from Experts

-

Single Payment Triggers: According to an article by Bankrate, just one missed payment can trigger actions from creditors regarding repossession. Although no fixed rule exists outlining the exact thresholds for missed payments, a single missed obligation poses a notable risk of repossession as it can alert creditors to potential payment issues. The immediate implication is a higher risk to the consumer’s credit standing and financial health.

-

Three Missed Payments: Experts from Experian highlight that missing 30 to 90 days of payments is a crucial threshold, after which creditors can consider the loan in default. This scenario may result in creditors initiating repossession procedures. Consequently, timely payments are emphasized as a means to sidestep significant legal and financial ramifications.

-

Accumulated Delinquencies: In a broader context, risks increase with missed payments, particularly if they accumulate. Financial Times experts suggest that even if individual payment failures might not seem consequential, they represent an important red flag that can influence not only the current loan terms but also future borrowing opportunities. Therefore, the cumulative effect of several missed payments can weaken a borrower’s position significantly in repossessing asset cases.

Conclusion

For fleet operators and business managers in industries reliant on vehicles, maintaining a consistent payment schedule is paramount. Missing more than one payment can escalate the risk of repossession, typically around three missed payments as identified by industry standards. This understanding reinforces the necessity of prompt communication with creditors if financial difficulties arise and establishing a robust financial management system to mitigate such risks.

For more insights on financial planning and management in the trucking industry, consider visiting our blog for expert advice and resources.

Preventive Measures to Avoid Repossession for Fleet Managers

As a fleet manager, effectively managing truck payments is crucial to ensuring the stability and success of your operations. Repossession can severely disrupt your business and damage your financial standing. To prevent such adverse events, implementing proactive management strategies is essential. Below are several actionable measures to help you stay ahead of potential payment issues:

1. Automate Payment Processes

Setting up automated payment systems can significantly reduce the risk of missed payments. By coordinating with your financial institution, you can arrange for payments to occur automatically on their due dates. This reduces the chances of human error and helps maintain a solid credit rating.

2. Regular Financial Audits

Conducting regular financial audits allows you to assess your fleet’s financial health. This practice involves reviewing all truck contracts, payment schedules, and outstanding debts. It can help identify potential issues early, giving you a chance to address them before they escalate into serious problems. Consider conducting these reviews quarterly or biannually.

3. Payment Tracking Software

Utilizing modern fleet management software can significantly enhance your ability to track payments. These systems can integrate payment scheduling, credit monitoring, and compliance alerts. A recent study showed that companies using such tools reduced payment delinquency by 68% and repossessions by over 70% (Transport Topics). Investing in a quality system can pay off substantially over time.

4. Driver Accountability

Engaging your drivers in the financial aspect of fleet management can be beneficial. Ensure they understand their role in reporting maintenance and operational issues that could lead to downtime. Early reporting can prevent unforeseen expenses that hamper payment capabilities. Create a culture of accountability where drivers feel responsible for vehicle upkeep and timely performance.

5. Establish a Contingency Fund

Establishing a contingency or emergency fund for your fleet can buffer against unforeseen expenses that might disrupt regular payment schedules. As recommended, having even a small financial cushion can relieve pressure during tough times or delays in cash flow (learn more about building an emergency repair fund).

6. Maintain Strong Communication with Financial Institutions

Keeping an open line of communication with your lenders can help manage expectations and facilitate timely resolutions of issues should they arise. Regularly discussing your financial standing and ongoing business operations can build trust and demonstrate your commitment to fulfilling your obligations.

Implementing these proactive strategies can greatly reduce the risk of missed payments and subsequent repossession of your trucks. By staying organized, leveraging technology, and engaging your team, you can ensure that your fleet remains on the road to success.

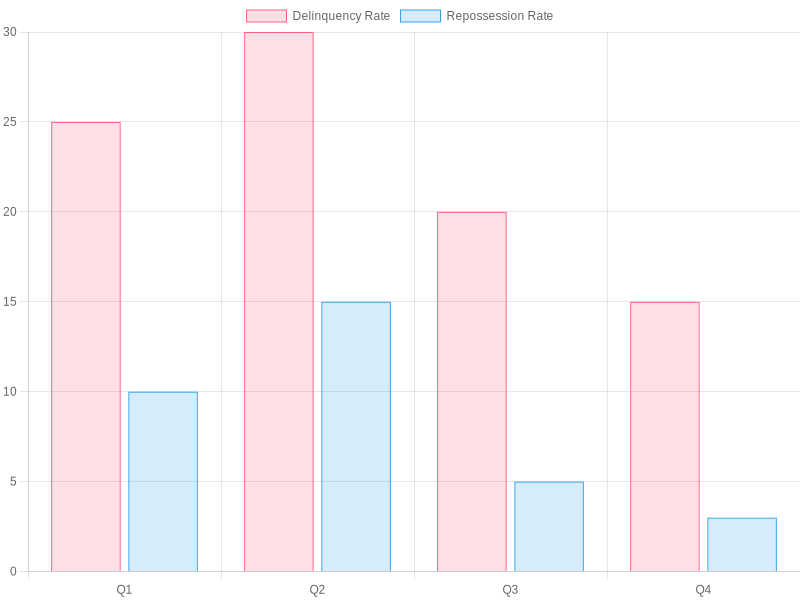

Impact of Fleet Management Software

To illustrate the effects of using fleet management software, refer to the graph below, which showcases the decline in delinquency and repossession rates after implementing such systems. This emphasizes the importance of transitioning to modern solutions in your fleet management practices.

Conclusion

By prioritizing proactive financial management and taking these actionable steps, fleet managers can significantly mitigate the risks of repossession and maintain a healthy fleet operation.

“Move your old ‘payment’ to a high-interest savings account every month. Keep driving. Keep saving. In about five years, walk in with cash.”

- John Doe, Financial Advisor

Managing truck payments diligently can prevent the risk of repossession, thereby preserving your business’s operational capacity and financial integrity.

Best Practices for Managing Truck Payments

Managing truck payments effectively is crucial for the financial health of your fleet. Here are some best practices to consider:

- Implement Automated Payment Systems: Use technology to automate payment processing, reducing errors and delays. This could involve integrating with billing and accounting software, such as QuickBooks.

- Real-time Reconciliation: Ensure real-time reconciliation of fuel cards, tolls, and invoices to maintain accurate financial records.

- Standardized Reporting Systems: Establish a daily reporting system where drivers log essential data, enhancing transparency and trust.

- Regular Audits: Conduct audits of payment records to identify discrepancies and ensure compliance with IRS regulations.

- Clear Payment Terms: Set clear payment terms with independent contractors to avoid disputes and maintain good relationships.

By incorporating these strategies, trucking companies can experience improved cash flow and financial stability. For more insights, see our articles on budgeting for routine truck maintenance and other topics in our blog.